The maritime industry relies heavily on the mortgage document known as the Preferred Ship Mortgage Form in the financing process. The lender certification is frequently encountered by vessel owners when obtaining loans and the registration of federally documented boats. A preferred mortgage ship creates a legally recognized security interest, which protects a lender’s interest while helping an owner obtain needed funding for the purchase, refinancing, or commercial operation of a vessel.

The documentation of a Federal vessel administers an official record that the United States Coast Guard keeps for the ownership of the property. To issue a large marine loan, lenders depend upon documented vessels that have a mortgage registered at the federal level, which offers better security than many state systems. If a mortgage is not recorded correctly, ownership disputes and financing issues may occur later.

A lot of recreational and commercial vessel owners misunderstand how preferred ship mortgages work. It is argued that the loan agreement alone sufficiently protects the lender. The mortgage filing officially records the lender’s interest in the federal vessel documentation records. The need for the legal recognition will arise in case of ownership disputes, default or refinancing, etc.

By knowing the preferred ship mortgage form, a boat owner will feel more confident. Preferred ship mortgages are how they work, why financiers require them, what are common financing scenarios, how do they operate alongside other financiers, and a few good tips on keeping accurate records of the mortgage.

Meaning of a preferred ship mortgage form

A secured legal interest exists in a ship that has federal documentation. The mortgage is recorded with the USCG by the lender in order to create a recordable lien on the boat.

Unlike other loan agreements, the federal documentation statutes grant preferred ship mortgages greater enforcement rights. Vessels with documentation are often preferred by lenders because the federal mortgage protection significantly lowers the financial risk.

| Feature | Preferred Ship Mortgage | Standard Marine Loan |

| Federal Recognition | Yes | Limited |

| Public Record Filing | Required | Varies |

| Lender Protection | Strong legal protection | Moderate protection |

| Used for Documented Vessels | Yes | Not always |

The term “federal vessel mortgage filing” comes up a lot during marine financing because lenders depend on official documentation records.

Preferred ship mortgages are used in many situations.

- Yacht-acquisition funding.

- Loans for ship.

- Refinancing deals for vessels.

- Transactions of large marine assets

The form of preferred ship mortgage helps with transparency of finance and accountability of ownership Mortgage records are reviewed by a variety of purchasers, lenders, insurers, and regulatory agencies.

To benefit commercial operators in Canada, lenders will offer more funds at lower interest rates when there is a federally recorded mortgage with strong enforcement provisions and legal protections. Structured financing for high value vessels is also offered owners for recreational use.

Federal mortgage filings stay on the record until paid off and released accurate mortgage recordation therefore has long term effects on ownership history and credit in finance.

Boat owners must know mortgage preference impact on resale deals. It is very important to keep accurate records as buyers regularly check mortgage status before purchasing a vessel.

A look at how preferred ship mortgages work in vessel financing

Frequent recreational purchases, marine funding techniques commonly happen for bigger loans. Due to the international mobility of vessels and their change in jurisdiction, lenders require more robust legal protections than personal loans generally offer.

Mortgage Document Submission

After approval of the finance terms, the lender registers the preferred ship mortgage against the documented vessel. By filing this document, an entry is created in the Coast Guard’s federal documentation records.

When a lender registers its mortgage, it protects its interest in the property against any subsequent disputes concerning ownership or against a default on payment. Prior to future transactions, buyers and other lenders may review these records.

The term “documented vessel financing” often shows up in marine loan parlance because federally documented vessels receive preferred mortgage treatment.

Obligations of Borrowers

The vessel owners have to follow the loan terms and keep a good status of their documentation. If you do not renew the documentation and comply with operational activities. You may face problems regarding financing.

- Agreement for preferred ship mortgage often requires.

- Current authorization of federal vessel.

- Repaying loans on time.

- Adequate protection for your boat.

Depending on the trade activities and operational category of the vessel, extra requirements will be laid for commercial operators.

Borrower Rights and Protections

When borrowers default, preferred mortgages give lenders strong legal protections. Since there is a federal recording of the mortgage, it would allow the lender to take action against the documented owner of the vessel.

The term “marine lender security interest” appears quite often in financing reviews. In most financing reviews, lenders usually rely on their basic mortgage enforcement rights quite heavily when advancing loan funds for larger vessels.

Satisfaction and Release of Mortgage

After the borrower has fully paid off the loan, the lender needs to file a satisfaction or release of mortgage. This filing effectively erases the lender’s financial claim from federal documentation.

Failing to document release can result in ambiguity regarding ownership. Boat owners should therefore ensure that the mortgage satisfaction reflects correctly on federal records after it has been paid off.

The lifecycle of the Preferred Ship Mortgage Form is from purchase to payoff and release. The preferred form remains important throughout the lifecycle.

Preferred Ship Mortgages Compared to Other Funding Choices

Frequently, boat owners compare their preferred ship mortgages with personal loans or state level marine finance arrangements. Despite the existence of various financing options, preferred mortgages offer distinct legal and operational advantages.

To enable successful farm operations, federal mortgage growing and servicing provides access to capital for farms and lending institutions. Usually, this structure results in better financing improvements for qualified borrowers.

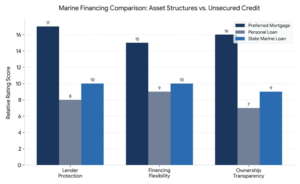

- The Preferred Ship Mortgage has a score of 17 for lender protection which is significantly better than State Marine Loan at 10 or Personal Loan at 8. The federal mortgage framework officially secures the debt against the vessel itself, giving rise to cross-border legal remedies.

- The structural flexibility of preferred mortgages scores 15 compared to 9 for personal loans and 10 state marine loans. Maximum financing flexibility The framework allows commercial operators to obtain complex, long-term repayment terms on high-value assets.

- Preferred Mortgages achieve a score of 16, demonstrating unmatched ownership transparency compared to Personal Loans at 7 and State Marine Loans at 9. This allows future purchasers and lenders to readily find active claims, and thereby reduce the risks of hidden transactions.

Summary: Preferred Ship Mortgages

The maritime sector can make use of the preferred ship mortgage form, to finance them. The preferred mortgage creates a more powerful legal claim through the recording of lender claim against federally documented vessels.

When vessels owners understand how preferred ship mortgages work, they will make better financing decisions. Filing accuracy, documentation organization and timely satisfaction of mortgages will help improve clarity of ownership and efficiency in transaction processes.

Federal mortgage recording provides especially significant value to commercial operators and higher-value vessel owners due to the heavy reliance by lenders on documented collateral protection. Accessible federal mortgage records provide advantages to buyers, insurers and financial institutions.

Marine financing is constantly changing in response to expanded vessel transactions globally. When owners carefully manage their mortgage records, they often have an easier time refinancing, transferring ownership, and negotiating with lenders.

The Preferred Ship Mortgage Form strengthens consumer confidence in the sale of vessels because claims on financing remain apparent on official registers until properly satisfied. In the boating sector, the long-term stability is being supported by this transparency.

Correctly preparing and maintaining preferred mortgage documents protects lenders and vessel owners throughout the financing life cycle. National Documentation E-Portal helps boat owners manage important documentation steps clearly for stronger operational success and financial flexibility.