The legalities pertaining to maritime and documentation law is imperative for the ownership, financing and regulatory compliance of vessels. It governs the documentation of vessels, the recording of the rights of ownership and the protection of interests in it. One of the crucial purposes of this legal system is the preferred ship mortgage. It gives lenders a secured interest while protecting owners through clear documentation.

Vessel owners must learn this area of law (maritime law). Discrepancies or misinterpretations can slow down financing, limit transfer or cause ownership dispute. Proper documentation makes it easier for lenders to enforce their claim and help them establish priority over other claims. Structured legal regulations and standardized processes achieve the balance between these interests.

This article describes the basic concepts of maritime and documentation law with a strong focus on preferred ship mortgages. It clarifies legal concepts in practical terms and explains the need to comply. This guide will provide clarity on how to tackle personal vessel financing, restructuring ownership, or planning for future transactions.

Maritime and Documentation Law is introduced

Vessels operating under national registries are governed by maritime and documentation law. It establishes identification, ownership and financing of vessels. Proper documentation provides the vessel with nationality as well as entitlement to the rights of a flag.

This law guarantees transparency of ownership records. Records allow authorities, lenders and buyers to verify one’s rights and obligations. Fleets might face operational and legal limitations without proper documentation.

One of the main features of this law is the preferred ship mortgage. Vessel owners can use it to get finance and lenders get enforceable rights. As opposed to informal agreements, these mortgages are recorded and prioritized under maritime law.

This system is important because it promotes predictability. Defined rules will lessen disputes and enhance investment on marine assets. When owners can get financing, lenders can be confident about enforcement.

| Legal Aspect | Documented Vessel | Undocumented Vessel |

|---|---|---|

| Ownership Clarity | High – Managed via a centralized federal registry with a clear chain of title. | Limited – Records are state-based and can vary in detail; prone to regional gaps. |

| Financing Options | Broad access – Lenders prefer federal status as it offers more security for high-value loans. | Restricted – Financing is often limited to personal loans or local bank credit with higher rates. |

| Mortgage Enforceability | Protected – Eligible for a “Preferred Ship Mortgage,” which has high priority in maritime law. | Uncertain – Lenders have fewer legal tools to seize or recover value in a default. |

| Regulatory Recognition | Full – Recognized internationally by foreign governments as a U.S. vessel. | Partial – Generally recognized only within the U.S. or specific state waters. |

This structure shows how proper documentation of the vessels is vital in the long run.

The Legal Structure and Requirements of a Preferred Ship Mortgage

The ship mortgage of choice is a key instrument of maritime and documentation law. With clear recordation for owners and authorities, it provides lenders with prioritized rights.

Legal base and precedence

Ship mortgage preferred status comes from proper registration but not from exclusive possession. When it is recorded, it will prevails over many other claims. This priority is crucial for lenders assessing risk.

The law prescribes rigid conditions for validity. There is accurate identification of the vessel Abstract and signatures being authorized. Any deviation may weaken enforcement.

Standards for compliance and documentation

Documents must be accurate for compliance. The small vessel details, ownership particulars and mortgage details must be compatible. Authorities will review submissions carefully to ensure legality.

The mortgage becomes effective upon acceptance and recording. Lender protections, however, remain limited for now. This stage highlights the importance of correctness.

Key compliance elements are

- The vessel should be clearly identified.

- Ownership records checked.

- Proper execution by authorized parties.

- Log with authority in time.

Every element aids enforceability and legal assurance.

A Comparison of Preferred Ship Mortgages and Other Security Interests

Realizing how preferred ship mortgages differ from other security interests is compelling. Traditional liens and private agreements offer less protection than this.

A statutory ship mortgage is recognized as a preferred ship mortgage. It enables enforcement by maritime courts. Additional contracts might entail intricate lawsuits.

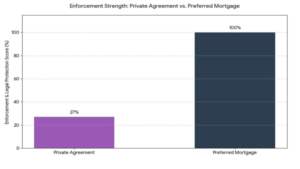

- Ironclad Legal Priority: A Preferred Ship Mortgage has a 100% enforceability because it is a federal lien and outranks nearly all other maritime claims. As a result, lenders always have the first right of recovery upon default.

- Federal Court Jurisdiction: Federal Court Jurisdiction: Preferred Mortgages Allow In Rem Actions in U.S. Federal Courts Unlike Private Agreements (27%) Which Often Lead to Messy State Litigation. The Federal Court gives approval for a vessel arrest to secure debt.

- Global Security Shield: Globally recognized under maritime treaties, a preferred mortgage means that the lender will be entitled to their interest even when the vessel is in foreign waters, which is not the case with private agreements.

- Public Record Integrity: Because the mortgage is recorded with the National Vessel Documentation Center (NVDC), it creates an Abstract of Title that stops the owner from selling the vessel without first satisfying the debt.

The image indicates tougher enforcement under maritime law. This strength focuses the mind on investing and financing.

Illustrative comparison scenario

Take two ships differently financed. One uses a favored mortgage and the other uses a private lien. The mortgage holder enforces their rights vigorously on default. The lien holder is being delayed and uncertain.

It is evident why they prefer maritime documentation. It helps the owners too by getting better finances.

Advice for Owners and Lenders

In-season maritime and documentation law requires preparation. Both owners and lenders must be aware of their responsibility. With proper planning we can reduce risk and delays.

Before financing, owners should check vessel eligibility. Accurate documentation means easier approval. Before disbursing funds, lenders must verify recording status.

Make sure to review all documents thoroughly. Make records consistent. Even small mistakes can result in lawsuits.

Inclusive best practices involve

- Verify the documentation before financing

- Accurately maintain ownership records

- Confirm monitoring recordings

- Certified copies of all legal filings must be retained

The above mentioned steps help you comply and safeguard long-term interests of the stakeholders.

Important Lessons on Key Maritime and Documentation Law

The law of maritime and documentation provides vessel ownership and financing legal framework. It ensures clarity and enforceability through proper rules and documented instruments. The primary ship mortgage is the basic element of this system.

Access to finance and clear ownership documents benefit the owners. National Documentation E‑Portal Lenders get priority and enforceable rights. Accurate documentation used by both parties to avoid dispute.

Awareness of these principles supports decisions. Correct compliance safeguards one’s investment and operations. When stakeholders adhere to the legal framework, trust and efficiency are enhanced.

This systematic method ensures the security, transferability, and title protection of maritime assets over time.